In partnership with

👋 Hi, it’s Rohit Malhotra and welcome to Partner Growth Newsletter, my weekly newsletter doing deep dives into the fastest-growing startups and S1 briefs. Subscribe to join readers who get Partner Growth delivered to their inbox every Wednesday morning.

Latest posts

If you’re new, not yet a subscriber, or just plain missed it, here are some of our recent editions.

Partners

Start learning AI in 2025

Everyone talks about AI, but no one has the time to learn it. So, we found the easiest way to learn AI in as little time as possible: The Rundown AI.

It's a free AI newsletter that keeps you up-to-date on the latest AI news, and teaches you how to apply it in just 5 minutes a day.

Plus, complete the quiz after signing up and they’ll recommend the best AI tools, guides, and courses – tailored to your needs.

Interested in sponsoring these emails? See our partnership options here.

Subscribe to the Life Self Mastery podcast, which guides you on getting funding and allowing your business to grow rocketship.

Previous guests include Guy Kawasaki, Brad Feld, James Clear, Nick Huber, Shu Nyatta and 350+ incredible guests.

S1 Deep Dive

Blend in one minute

Blend Labs is a cloud-based banking software provider on a mission to simplify financial services. Founded in 2012 by Nima Ghamsari, the company aims to make applying for a mortgage or opening an account as seamless as an online checkout.

The San Francisco-based firm filed for a $100M placeholder IPO, with Goldman Sachs leading the offering. It trades under the ticker symbol “BLND,” joining a wave of recent software IPOs, including Confluent, WalkMe, Squarespace, and Monday.com.

Blend powers digital-first consumer banking for mortgages, home equity loans, credit cards, and personal loans. It plans to expand into commercial banking. Its acquisition of Title365, a title insurance agency, for $422.1M is a major step in that direction. Title365 generated $212.1M in revenue in 2020—more than twice Blend’s $96M.

The financials are a study in high growth. Blend’s revenue surged 90% in 2020, with Q1’21 accelerating to 104% year-over-year. The company’s implied ARR sits at $124.3M, up 106%. Still, margins remain deeply negative, with non-GAAP operating margin at (73)% last quarter. Blend has raised $710.5M in equity, including a $310M Series G at a $3.3B valuation in early 2021. To fuel growth, it secured a $225M term loan and a $25M revolving credit facility.

Like many fintech disruptors, Blend is betting on scale. With 291 customers—18 of whom pay more than $1M annually—the company’s success hinges on driving transaction volume. A pricing model tied to completed transactions means seasonality plays a role, but Blend’s dollar-based net retention rate of 179% signals strong customer expansion.

For a deeper dive into Blend’s product strategy, competitive positioning, and the risks ahead, keep reading.

Introduction

Blend Labs doesn’t just build banking software—it’s reimagining the way financial services work. Founded in 2012 by Nima Ghamsari, the company set out to strip away the complexity of mortgages, loans, and bank accounts. The goal? Make applying for financial products as simple as checking out on Amazon.

That vision has propelled Blend into a dominant position. Today, it powers consumer banking journeys for mortgages, home equity loans, credit cards, and more. Banks, credit unions, and fintech startups alike rely on Blend’s cloud-based platform to modernize their offerings. Soon, commercial banking will be part of the mix.

Traditional banks are constrained by outdated systems. Digital-native challengers are luring customers away. Blend is the middle ground—giving legacy institutions the agility of a startup without the tech headaches. And the numbers show it's working. In 2020, financial firms processed $1.4 trillion in loan applications through Blend. The company’s ecosystem of 2,200+ partners has grown 1,300% year-over-year, forming a marketplace that spans realtors, insurers, and service providers.

Unlike traditional SaaS, Blend’s pricing model is transactional. No fees for abandoned applications. Revenue comes from completed transactions—funded loans, new accounts, finalized deals. It’s a high-risk, high-reward model that ties Blend’s fate to its customers’ success. Last year, 18 clients generated over $1M each for Blend, making up more than half of its revenue.

There’s a reason banks are betting big on Blend. The platform doesn’t just digitize banking—it rewires it for a world where convenience is king. That’s why institutions like Wells Fargo, Truist, and U.S. Bank have signed on. That’s why Blend is expanding into commercial banking. And that’s why it filed for a $100M IPO.

History

In 2012, Nima Ghamsari, alongside co-founders Rosco Hill, Eugene Marinelli, and Erin Collard, established Blend Labs, Inc., aiming to infuse simplicity and transparency into financial services by streamlining processes like mortgage applications and account openings.

Over the years, Blend has developed a comprehensive suite of white-label products, facilitating digital-first consumer experiences across various financial services, including mortgages, home equity loans, vehicle loans, personal loans, credit cards, and deposit accounts.

In March 2021, Blend expanded its capabilities by acquiring Title365, a title insurance agency, for $422.1 million. This strategic move aimed to enhance Blend's service offerings in the title insurance domain.

The company went public on July 22, 2021, trading under the ticker symbol "BLND" on the New York Stock Exchange, with an initial public offering price of $18 per share.

As of December 31, 2023, Blend reported annual revenues of $156.85 million, with a workforce comprising approximately 881 employees.

Today, Blend continues to innovate, providing digital lending solutions to over 250 financial institutions across the United States, including top banks and credit unions, thereby transforming the consumer banking experience.

Risk factors

Blend Labs has been on a steep growth trajectory, but the road ahead looks different. After nearly doubling revenue from $50.7 million in 2019 to $96 million in 2020, the company expects its growth rate to slow. As Blend expands, maintaining rapid revenue gains will become more challenging.

Sustaining momentum hinges on several factors—retaining customers, increasing transaction volumes, and expanding product offerings. Pricing will be critical. Blend needs to attract and retain financial institutions without undercutting profitability. The company has also made aggressive bets, including its $422 million acquisition of Title365, a move that could fuel growth or strain resources.

Despite its progress, Blend remains unprofitable. The company has recorded net losses every year since its founding in 2012, with a $74.6 million net loss in 2020 alone. Operating at this scale isn’t cheap. Costs will continue to rise as Blend invests in product development, sales, and customer support. Even with strong revenue growth, there’s no guarantee the company will reach profitability anytime soon.

Blend’s business model also introduces risk. A small number of key customers account for a significant portion of revenue. If any of them scale back or leave, Blend’s growth could take a hit. Meanwhile, competition is heating up. Traditional banks, fintech challengers, and in-house solutions all threaten Blend’s market share.

The company’s success will depend on execution. If Blend can continue expanding its customer base and transaction volume, it could cement itself as a key player in digital banking. But if customer adoption slows or market conditions shift, the path to profitability could become even more elusive.

Market Opportunity

The financial services software market is enormous, and Blend sees itself positioned across several key spending categories. Banks, lenders, and insurers are pouring billions into IT infrastructure, title and home insurance, and real estate transactions—areas where Blend is making a play.

The numbers speak for themselves. Gartner estimates global banking IT software spend hit $72.4 billion in 2020, with projections of a 13% compound annual growth rate (CAGR) through 2025. Title insurance premiums in the U.S. alone totaled $19.2 billion that same year, according to the American Land Title Association. Home insurance is even bigger—IBISWorld reports that U.S. consumers spent $105.7 billion on home insurance premiums in 2020.

And then there’s real estate. Blend estimates that $123.5 billion was spent on realtor commissions in 2020, drawing from data compiled by the National Association of Realtors, EffectiveAgents.com, and the St. Louis Federal Reserve.

Blend’s total addressable market (TAM) is a reflection of these massive industries. By focusing on the transactions powering consumer banking and home financing, the company estimates its slice of the market at $33 billion+.

The opportunity is clear—but so is the competition. Banks and fintechs are fighting for market share, and enterprise IT budgets are increasingly tied to in-house solutions. Blend is betting that its software platform will serve as the connective tissue between these financial services, helping legacy players modernize while taking a cut of the transaction flow.

Product

Blend is building the connective tissue for modern consumer banking. Its suite of white-label products powers digital-first lending and banking experiences, streamlining processes for mortgages, home equity loans, vehicle loans, personal loans, credit cards, and deposit accounts. These aren’t just bolt-on solutions—they act as the digital interface between banks and consumers, a critical touchpoint in financial services.

The core of Blend’s offering is modularity. The platform is built from a library of low-code components, assembled into workflows using its “Journey Builder.” Each module tackles a key part of the lending process:

Verification – Identity, asset, income, and credit checks

Decisioning – Pre-approvals, cross-selling, and rule-based logic

Workflow Intelligence – Data collection and automation

Marketplaces – Seamless integrations with third-party services like real estate agents and insurance providers

This structure allows financial institutions to configure lending journeys to fit their needs without deep technical expertise.

Blend’s flagship products cover a range of financial transactions:

Mortgage – A fully digital mortgage process, from application to closing.

Home Equity – Faster home equity loans and lines of credit.

Vehicle Loan – Quick financing for cars, boats, RVs, and more.

Credit Card – Higher application conversions through streamlined workflows.

Personal Loan – Automated pre-approvals for unsecured and secured loans.

Deposit Account – Fraud prevention tools designed for financial compliance.

Beyond lending, Blend is expanding its footprint into property and casualty insurance and title insurance, verticals that naturally integrate into its ecosystem. The company’s acquisition of Title365 brings not just a title insurance platform but a network of 7,000 notaries, reinforcing its position in home financing.

The scale of Blend’s ecosystem is a major differentiator. The company now boasts 2,200+ partners, a 1,300% year-over-year increase. This network includes technology providers, data aggregators, and financial service partners, all designed to enhance the consumer banking experience.

In essence, Blend is betting that financial services should be as seamless as online shopping. Whether it can execute on that vision—and fend off growing competition—will determine its long-term success.

Partners

Amplify Labs partners with founders, CEOs, and busy professionals to build authority, generate leads, and grow audiences across LinkedIn, X (formerly Twitter), and newsletters.

We specialize in crafting high-performing written content tailored to your unique voice, goals, and niche—helping you stand out and become a go-to expert in your industry. One of our clients generated 50+ qualified leads from a single post. Another landed inbound interest from a multibillion-dollar company.

Interested in sponsoring these emails? See our partnership options here.

Business Model

Blend’s revenue model is built to align with its customers. The company charges fees based on completed transactions—funded loans, new account openings, or closings—rather than abandoned applications. Transaction fees remain flat regardless of loan size, but customers receive volume-based discounts when they reach certain thresholds. Blend also offers contract minimums, a model that accounted for 12% of revenue in 2019 and 2020, effectively functioning as an annual subscription. The company expects to expand its revenue streams through commissions and service fees on its growing marketplace.

Sales & Customer Base

Blend operates on a direct sales model, with long sales cycles typical for enterprise deals. Smaller lenders take 6-9 months to close, while larger institutions require 12-18 months. However, once a customer is onboarded, adding additional products is faster—a critical factor in driving expansion revenue.

The business is also seasonal, with Q2 and Q3 seeing higher transaction volumes, driven by peak mortgage demand in the summer months. All of Blend’s 291 customers (as of 2020) are U.S.-based, spanning large banks (Wells Fargo, U.S. Bank), credit unions, fintechs, and non-bank mortgage lenders.

By the Numbers: Blend’s Growth

$1.4T in loan applications processed in 2020, up from $540B in 2019

190% increase in completed banking transactions from 2019 to 2020

31 of the top 100 U.S. financial services firms use Blend

$5B+ in daily loan volume processed

36% of full-time employees focused on R&D, with weekly product updates

$165M+ invested in R&D since 2015

9/10 median rating from consumers for Blend’s user experience

1 issued patent in the U.S., with pending patents in Europe, Canada, and Australia

Expanding the Ecosystem

Blend isn’t stopping at lending. The company has built a licensed property and casualty insurance agency operating in all 50 states and has signed an agreement to acquire Title365, one of the largest U.S. title insurance agencies. Title365 brings 7,000 notaries into Blend’s ecosystem, strengthening its position in end-to-end mortgage processing.

Industry Trends Supporting Blend

30% increase in mobile banking adoption during COVID-19 (Boston Consulting Group)

53% of consumers prefer bundled services (e.g., mortgage + real estate or auto loan + dealership offer) (Deloitte)

42% of U.S. consumers use fintechs, and switching rates are rising (McKinsey)

48% of banks & 42% of credit unions have partnered with fintechs in the last three years, with 86% prioritizing customer experience (Cornerstone Advisors)

$447B in potential cost savings for financial firms from automation by 2030 (Autonomous Research)

Blend sits at the intersection of these macro trends. Its platform is designed for a financial world that prioritizes seamless digital experiences, embedded services, and automation. The question is—can it maintain its momentum as competition intensifies?

Management Team:

Blend’s leadership team is a mix of founders, industry veterans, and financial experts. The company’s executive team is anchored by co-founder Nima Ghamsari, while the board includes a former Federal Reserve Vice Chairman and key figures from venture capital and finance.

Executive Team

Nima Ghamsari (35) – Head of Blend, Co-Founder, and Director

Ghamsari co-founded Blend in 2012 and has led the company since its inception. Prior to Blend, he worked at Palantir Technologies as a software engineer. Ghamsari holds a B.S. in Computer Science from Stanford University. His early experience building data-driven platforms at Palantir laid the foundation for Blend’s product-first approach.

Timothy J. Mayopoulos (62) – President and Director

Mayopoulos joined Blend in 2019 after a six-year stint as the CEO of Fannie Mae (2012–2018), where he guided the mortgage giant through a post-crisis recovery. He previously held senior positions at Bank of America, Deutsche Bank, Credit Suisse First Boston, and Donaldson, Lufkin & Jenrette. Mayopoulos also sits on the boards of SAIC and LendingClub. His deep ties in financial services give Blend a significant edge in working with large financial institutions.

Marc Greenberg (50) – Head of Finance and Head of People

Greenberg has led Blend’s finance operations since 2018 and added the Head of People role in 2020. Before Blend, he spent over 15 years at Pixar Animation Studios, where he served as Vice President of Finance and Strategy. Greenberg holds a B.S. in Business and Management from the University of Maryland. His dual role reflects the growing importance of both financial and human capital at Blend.

Crystal Sumner (37) – Head of Legal, Compliance, and Risk; Corporate Secretary

Sumner has been with Blend since 2016, overseeing legal, compliance, and regulatory affairs. Before Blend, she was Product and Regulatory Counsel at Eventbrite and an Enforcement Attorney at the Consumer Financial Protection Bureau (CFPB). Sumner holds a J.D. from UC Berkeley and a B.A. in International Business from Texas Tech University. Her CFPB background is critical as Blend navigates the highly regulated financial services sector.

Investment

Blend has raised $710.5M in equity financing, according to the S-1, with backing from some of the most influential names in venture capital. The company’s investor list reads like a who’s who of Silicon Valley: Lightspeed, Formation8, Coatue, Tiger Global, Greylock, General Atlantic, Temasek, Emergence, Fifth Wall, and Andreessen Horowitz (a16z) all hold positions.

The most recent raise was a $310M Series G in January 2021 led by Coatue and Tiger at a $3.3B post-money valuation (share price of $4.61). That same month, Coatue and Tiger facilitated a tender offer to purchase Series A shares at $4.15 per share, totaling $5.5M.

Co-founder and CEO Nima Ghamsari holds an 8.8% pre-offering stake—but his control extends beyond that. Blend has a dual-class stock structure where Class A common stock (the shares being offered in the IPO) carries one vote per share, while Class B common stock holds 40 votes per share. Ghamsari owns all the Class B shares, giving him full voting control post-IPO.

Lightspeed’s 12.5% stake alone could be worth $400M+ at a $3.3B valuation—an impressive return even by Silicon Valley standards. Coatue and Tiger’s decision to double down through the tender offer underscores their confidence in Blend’s market position and future growth.

Competition

The competitive landscape for financial services software is heating up, but Blend’s positioning is unique. While the company doesn’t directly name competitors in its S-1, the broader market for banking and lending software is highly competitive, with both horizontal platforms and vertical solutions vying for market share.

Point Solutions

At the most basic level, Blend competes with point solution vendors that specialize in specific areas like mortgage origination, loan processing, and customer verification. These point solutions are typically built for a narrow use case and optimized for a single product or customer segment. While they may offer deep functionality, their lack of platform breadth limits their ability to scale across different financial products. Blend’s ability to integrate multiple solutions under one platform gives it an edge over these niche players.

Back-Office Software

Many financial institutions rely on a patchwork of back-office software and internally developed systems to manage lending operations. These systems are often highly customized and deeply embedded into a bank’s infrastructure, making them difficult to replace. However, they tend to be clunky, expensive to maintain, and slow to adapt to changes in consumer behavior. Blend’s strength lies in offering a modern, cloud-based alternative that unifies the lending process under a single interface.

Market Movers

The biggest shift in the market has come from strategic acquisitions and consolidations:

ICE (Intercontinental Exchange) acquired Ellie Mae for $11B in 2020—just over a year after Thoma Bravo bought Ellie Mae for $3.7B. This underscores the growing value of digitized mortgage platforms and the strategic importance of controlling the underlying infrastructure.

Qualia, a real estate closing platform, is another fast-growing player in the space. Its rapid rise suggests strong demand for end-to-end digitization in real estate transactions—a trend that Blend is well-positioned to capitalize on with its expanding suite of products.

Ecosystem and Scale

Blend’s key differentiator is its ability to offer a multi-product platform that scales across different financial products and integrates with external partners. The company’s growing ecosystem—spanning 2,200 partners and including more than 45 technology providers and 1,200 marketplace partners—creates network effects that make it harder for competitors to displace Blend once embedded.

Blend’s platform isn’t just about processing loans—it’s about owning the relationship between the financial institution and the consumer. Much like how Atlassian built a strong moat through developer loyalty with Jira, Blend is creating a similar dynamic within the financial services industry. The breadth of Blend’s product suite and its deep ecosystem make it less vulnerable to point solutions or back-office competitors—and more positioned to define the future of digital lending.

Financials

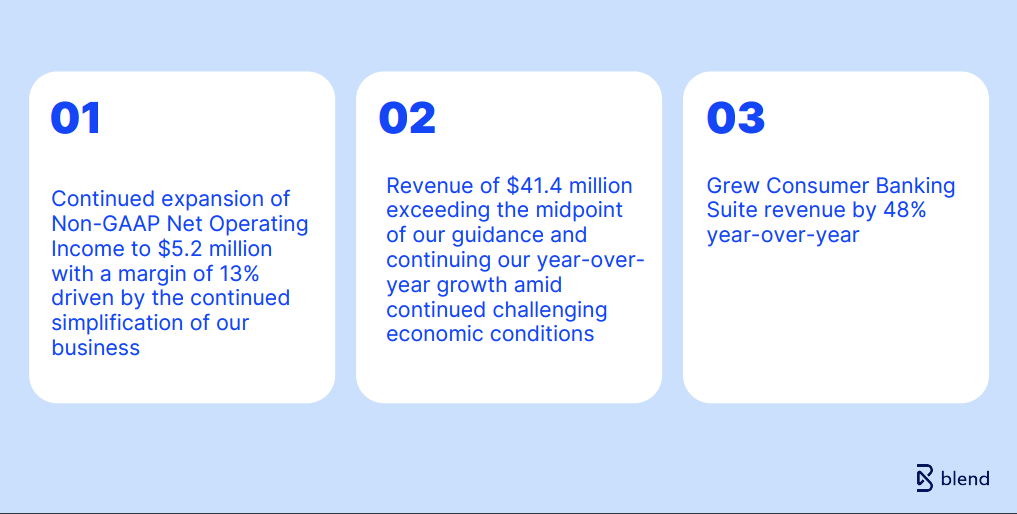

Blend reported Q4 2024 revenue of $41.4 million, which exceeded the midpoint of its guidance and reflected a 15% year-over-year (YoY) increase from Q4 2023 ($36.1 million). The growth was driven by a strong performance in the Consumer Banking Suite and the Mortgage Suite despite challenging economic conditions.

Consumer Banking Suite Revenue:

Reached $9.5 million in Q4 2024, up 48% YoY from $6.4 million in Q4 2023.

Contributed 31% of total platform revenue, up from 25% in Q4 2023.

Mortgage Suite Revenue:

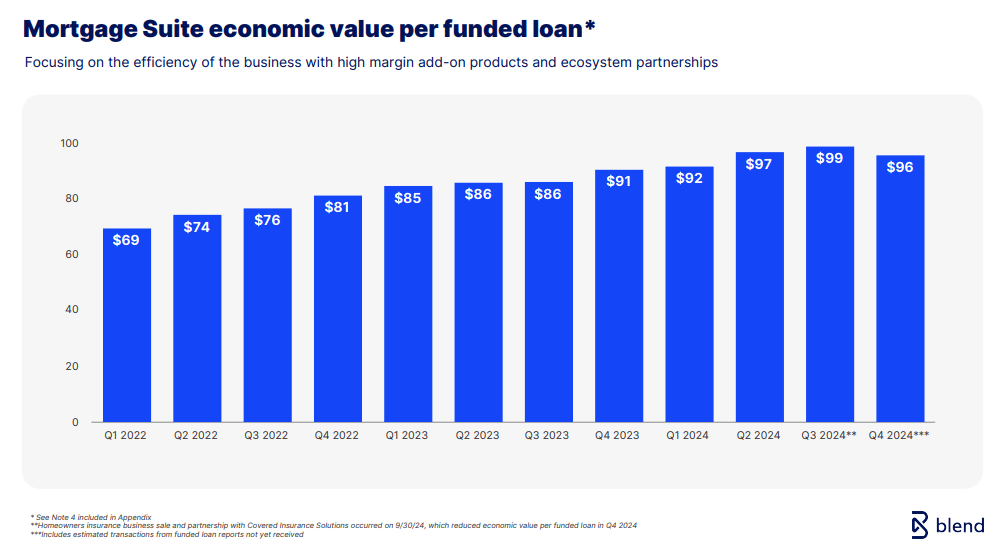

Delivered $18.2 million in Q4 2024, down 6% YoY from $17.2 million in Q4 2023.

Mortgage market softness is likely a factor, as the number of originations decreased industry-wide.

Professional Services:

Generated $2.5 million in Q4 2024, up 10% YoY from $2.3 million in Q4 2023.

Represents a relatively small portion of the business (~8% of revenue).

Title Business:

Title-related revenue increased by 10% YoY to $11.3 million in Q4 2024, up from $10.2 million in Q4 2023.

Total 2024 revenue reached $162.0 million, representing a 3% increase from $156.8 million in 2023. While this is modest overall growth, the strong performance in consumer banking partially offset headwinds in the mortgage business.

Profitability and Margins

Blend reported an improving profitability profile:

Non-GAAP Gross Margin:

Consolidated non-GAAP gross margin improved to 61% in Q4 2024, up from 55% in Q4 2023.

Blend Platform's gross margin rose to 75% from 71% YoY, reflecting improved operational efficiency.

Non-GAAP Operating Income:

Blend achieved a positive non-GAAP operating income of $5.2 million in Q4 2024 (13% margin) — a sharp turnaround from a $13.1 million loss in Q4 2023.

This was driven by reduced operating expenses, increased transaction volume, and stronger monetization.

Net Loss:

GAAP net loss improved significantly to $708K in Q4 2024, down from a $30.4 million loss in Q4 2023.

On a full-year basis, net loss was $43.4 million in 2024 versus $179.9 million in 2023 — an improvement of over 75%.

Operating Expenses

Blend has made meaningful progress in cutting costs and improving operating efficiency:

Sales and Marketing:

Non-GAAP sales and marketing expense was $5.5 million in Q4 2024, down 49% YoY from $10.9 million in Q4 2023.

Reflects the exit from the Homeowners Insurance business and partnership with Covered Insurance Solutions (~$1.3 million reduction).

Research and Development:

Non-GAAP R&D expense was $6.9 million, down 42% YoY from $11.8 million in Q4 2023.

Represents a strategic shift toward focusing on high-margin products and platform improvements.

General and Administrative:

Non-GAAP G&A expense was $7.5 million, down 27% YoY from $10.3 million in Q4 2023.

Cost savings from workforce reductions and facilities restructuring contributed to the decline.

Total non-GAAP operating expenses fell to $19.9 million in Q4 2024, down 39% YoY from $32.9 million in Q4 2023.

Cash Flow and Liquidity

Blend’s cash flow improved significantly:

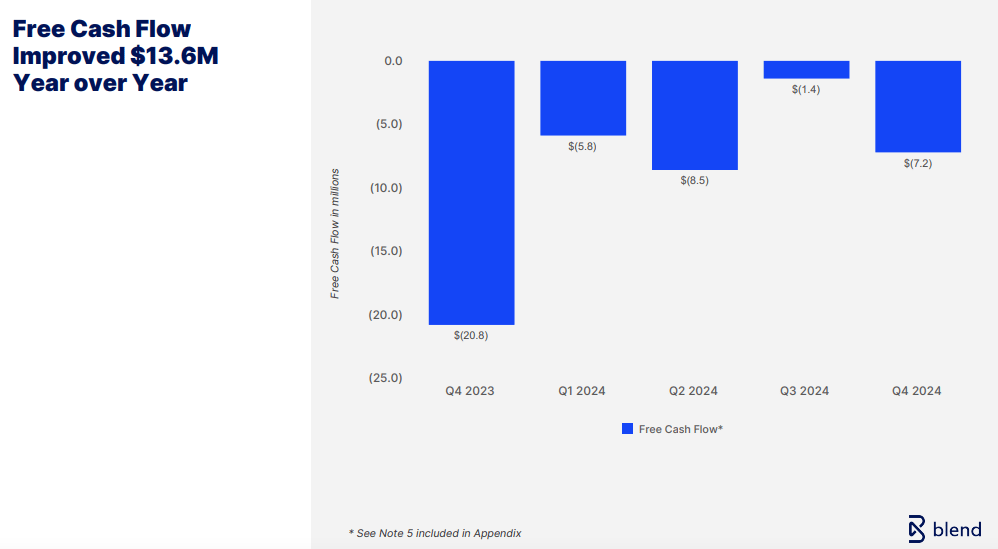

Free Cash Flow:

Free cash flow improved by $13.6 million YoY.

Q4 2024 free cash flow was ($7.2) million, a notable improvement from ($20.8) million in Q4 2023.

Unlevered Free Cash Flow:

Improved to ($7.2) million in Q4 2024 from ($14.4) million in Q4 2023, reflecting better cost management.

Customer Expansion and Retention

Dollar-Based Net Retention Rate:

Ended 2024 at 179% — a strong indicator of Blend’s ability to grow with existing customers.

Growth is driven by cross-selling more products within the platform.

Customer Cohort Growth:

Customers acquired in 2018 generated 2.9x revenue in 2020.

Customers acquired in 2019 generated 3.0x revenue in 2020.

Indicates Blend's ability to drive deeper customer engagement over time.

Blend’s financial profile is typical of a fast-growing SaaS company focused on long-term market dominance over short-term profitability. The company is scaling quickly, driving high retention and strong revenue growth—but the key to future success will be balancing growth investments with improving unit economics.

Closing thoughts

Blend’s Q4 2024 results underscore a company that is effectively navigating a complex and competitive financial services landscape. Revenue reached $41.4 million, up 15% YoY, driven by strong growth in the Consumer Banking Suite, which increased 48% YoY to $9.5 million. This shift toward consumer banking signals Blend’s success in diversifying beyond mortgages and expanding its total addressable market. Importantly, profitability has improved significantly. Blend achieved a positive non-GAAP operating income of $5.2 million (13% margin) — a stark turnaround from a $13.1 million loss a year ago. Operating expenses declined by 39%, driven by reduced sales and marketing costs and increased operational efficiency. Gross margins expanded to 61%, reflecting improved monetization and better cost control.

The company’s 179% dollar-based net retention rate highlights strong customer expansion within existing accounts — a clear indicator of product-market fit and cross-sell success. Despite softness in the mortgage market, Blend’s ability to drive adoption in consumer banking and professional services positions it well for continued growth. The company expects 35% to 40% growth in Consumer Banking Suite revenue in 2025, pointing to strong momentum. While macroeconomic factors could introduce headwinds, Blend’s expanding product suite, improving profitability, and growing customer base suggest it is well-positioned to sustain long-term growth.

Here is my interview with Jenny Fielding, the co-founder and Managing Partner of Everywhere Ventures. She is the author of the book, Venture Everywhere

In this conversation, Jenny and I discuss:

What do most founders think they know about fundraising but do not?

What’s unique about the female founder ecosystem in venture capital?

What are some of the unique challenges and opportunities Jenny has observed in global startups outside of Silicon Valley?

What inspired Jenny to write “Venture Everywhere”

If you enjoyed our analysis, we’d very much appreciate you sharing with a friend.

Tweets of the week

Here are the options I have for us to work together. If any of them are interesting to you - hit me up!

Amplify Labs: We help you grow your audience on LinkedIn, X (formerly Twitter), and newsletters.

Sponsor this newsletter: Reach thousands of tech leaders

Upgrade your subscription: Read subscriber-only posts and get access to our community

Subscribe to my YouTube channel: Your Learning Playground with over 350+ podcasts. Previous guests include Guy Kawasaki, Brad Feld, James Clear, and Shu Nyatta.

And that’s it from me. See you next week.