👋 Hi, it’s Rohit Malhotra and welcome to Partner Growth Newsletter, my bi-weekly newsletter doing deep dives into the fastest-growing startups and S1 briefs. Subscribe to join readers who get Partner Growth delivered to their inbox every Wednesday and Friday morning.

Latest posts

If you’re new, not yet a subscriber, or just plain missed it, here are some of our recent editions.

Subscribe to the Life Self Mastery podcast, which guides you on getting funding and allowing your business to grow rocketship.

Previous guests include Guy Kawasaki, Brad Feld, James Clear, Nick Huber, Shu Nyatta and 350+ incredible guests.

S1 Deep Dive

Affirm in one minute

Affirm Holdings, founded in 2012 by PayPal co-founder Max Levchin, is a disruptor in the Buy Now, Pay Later (BNPL) market, bringing transparency and simplicity to consumer credit. Affirm’s model offers point-of-sale loans with fixed payments, no hidden fees, and no late charges—a stark departure from traditional high-interest credit products. For Affirm, clarity isn’t just a feature; it’s a core philosophy.

The company’s growth story is tied to strategic partnerships with retail giants like Walmart, Shopify, and Peloton. These alliances powered $2.3 billion in revenue in 2024, reflecting a 28% year-over-year surge. Yet, Affirm’s success has come with trade-offs. It remains unprofitable, posting consistent net losses, though its cash flow and liquidity provide a sturdy financial backbone. The company serves over 4 million active subscribers, expanding its reach in a rapidly evolving global market.

Affirm’s challenge lies in proving that its user-first approach and financial accessibility can translate into sustained profitability, especially amid fierce competition. But its commitment to reshaping consumer credit for a new generation—and its bold stand on transparency—makes it a defining player in the digital finance landscape.

Stock Overview:

Stock Price: $55.81

Market Cap: $17.34B

52 Week High: $73.34

52 Week Low: $22.25

For more on Affirm’s approach, its competitive edge in the BNPL space, and the road to profitability, keep reading.

Introduction

It wasn’t the dawn of a new financial era, but Affirm wanted you to believe it could be. The Buy Now, Pay Later pioneer had grown to represent more than just a payment option—it was a philosophy.

“Affirm isn’t a loan company,” its founder Max Levchin might argue. “It’s a promise.”

In some ways, that promise—of transparency, empowerment, and financial simplicity—redefined how consumers thought about credit. Gone were the days of hidden fees and ballooning interest rates; Affirm offered point-of-sale financing that was clear, predictable, and above all, humane. It wasn’t just about borrowing money; it was about building trust.

Levchin, known for co-founding PayPal, is far from the type of founder who dazzles with theatrical bravado. Quiet, methodical, and relentlessly focused, he instead embodies the spirit of his company. Affirm’s mission wasn’t wrapped in Silicon Valley’s usual hyperbole; it was straightforward: financial products that treat people like people.

And yet, the ambitions behind Affirm have a whiff of something larger. To believe in Affirm is to believe in a future where consumer credit is not just a transaction but a tool for empowerment. Where a company’s success is measured not only in dollars and growth but in the trust it earns along the way.

The question is whether trust alone can be the moat Affirm hopes it is. What is transparency worth in a crowded market where rivals race to capture consumers and profits remain elusive? Keep reading to explore how Affirm is betting it can build a state of consciousness—one payment at a time.

History

Does the name Max Levchin ring a bell? If so, it probably conjures images of PayPal, Silicon Valley, and the early days of online payments. And that makes sense. As a co-founder of PayPal, Levchin helped redefine how we transact online.

But if we look at Levchin's career holistically, PayPal is only the prologue. After revolutionizing payments in the early 2000s, the Ukraine-born entrepreneur turned his sights to an even loftier ambition: making credit simple, fair, and transparent. In 2012, he founded Affirm.

A fintech veteran with an engineering mindset, Levchin believed the traditional credit system was broken—laden with compounding interest, hidden fees, and consumer distrust. His solution was bold in its simplicity: build a product that puts transparency first. Affirm wasn’t just a financial tool; it was a promise to treat consumers like humans.

The company’s big break came with partnerships that turned heads. Peloton and Expedia weren’t just customers—they were proof points. Affirm enabled big-ticket purchases with low-cost, flexible financing, benefiting both merchants and buyers. By 2020, what started as a payment solution had grown into a full BNPL ecosystem, complete with a consumer app, merchant integrations, and advanced fraud detection.

What’s remarkable about Affirm isn’t just its scale or growth—it’s the cultural shift it represents. Levchin didn’t just build another fintech product; he built trust into a market long dominated by skepticism. In the years since, Affirm has become more than a company. It’s a case study in how fintech can blend innovation and humanity, reshaping consumer credit for the modern age.

Market Opportunity

Affirm’s moment is here. As consumer behavior shifts away from traditional credit systems and toward transparency-first, tech-enabled financial solutions, the company sits at the crossroads of a generational transformation. Affirm isn’t just riding a trend; it’s defining it.

E-commerce: The Catalyst for Growth

Global e-commerce, a juggernaut reshaping retail, is the foundation of Affirm’s success. From $4.2 trillion in 2020 to a projected $8 trillion by 2026, e-commerce is growing at a 12% CAGR. Affirm’s role in this ecosystem is clear: turning browsers into buyers by bridging the gap between cart and checkout. With its seamless "Buy Now, Pay Later" (BNPL) solutions, Affirm empowers merchants and consumers alike, offering flexibility that aligns with modern financial priorities.

Younger consumers are driving this shift. Millennials and Gen Z, who value clarity and control in their financial lives, are ditching credit cards for alternatives like BNPL. This alignment of consumer preference and Affirm’s value proposition sets the company apart as e-commerce evolves.

COVID-19: The Accelerant

If e-commerce was a rocket, COVID-19 was the booster engine. In 2020, the pandemic accelerated digital adoption, pushing e-commerce’s share of U.S. retail sales from 16% to 21% in months. Alongside this shift came a surge in demand for BNPL services, with Affirm positioned as a key player for consumers seeking financial flexibility during uncertain times.

BNPL: A $3.2 Trillion Revolution

The BNPL market, valued at $120 billion in 2020, is on track to reach $3.2 trillion by 2030, with a staggering 43% CAGR. Affirm’s approach—offering fixed payments without hidden fees—resonates deeply with digital-first consumers. Merchants, too, are seeing the impact, reporting up to 92% increases in Average Order Value (AOV) and improved conversion rates.

The Shopify Effect

One partnership underscores Affirm’s strategic vision: Shopify. In 2020, Affirm became Shopify’s BNPL provider, giving it access to the platform’s $175 billion in annual GMV. This integration positions Affirm to tap into a projected $250 billion market opportunity by 2025, leveraging Shopify’s vast merchant network as e-commerce continues to thrive.

Expanding Horizons

Affirm’s opportunity isn’t limited to high-ticket items like fitness equipment or travel. Everyday essentials—groceries and routine purchases—represent a potential $1 trillion annual market in the U.S. alone. Affirm’s products, like Split Pay, are designed to unlock this segment’s potential.

Geographically, Affirm’s growth is just beginning. While its North American TAM stands at $680 billion, global markets could expand that to over $2 trillion, with high adoption rates in Europe, Australia, and Asia.

Future Verticals: Healthcare and Education

Beyond retail, Affirm is eyeing new frontiers. Rising healthcare costs create an opportunity to offer financing for medical expenses, a $350 billion market. Similarly, education financing for boot camps and online courses presents a $200 billion market ripe for disruption.

Affirm’s mission is bold: to redefine consumer credit for a new generation. With a rapidly growing TAM, strong merchant partnerships, and a unique approach to transparency, Affirm is more than a player in the BNPL market—it’s a leader.

The question isn’t whether Affirm can grow, but how far it can go in reshaping financial norms. This is a company not just transforming commerce but rethinking how trust and technology intersect in the financial world.

Product

Affirm serves as a financial orchestrator, bridging consumers and merchants with its versatile product ecosystem designed to make credit more transparent and accessible. While the "Buy Now, Pay Later" (BNPL) model remains Affirm’s flagship offering, the company’s broader suite of tools positions it as a cornerstone in the evolving commerce landscape.

At its core, Affirm redefines the relationship between credit and trust, emphasizing simplicity, clarity, and flexibility in every transaction.

The Consumer Experience

For consumers, Affirm’s mission is clear: eliminate the stress and opacity of traditional credit systems. Its products are built to offer seamless financing options while putting users in control of their financial decisions.

Point-of-Sale Financing

Affirm’s hallmark product is its Point-of-Sale (POS) financing, allowing consumers to pay for purchases in manageable installments directly at checkout.

0% APR Plans: For eligible purchases, Affirm offers no-interest payment options, subsidized by merchant partnerships.

Simple Interest Loans: For interest-bearing loans, users pay only the fixed amount disclosed upfront—no compounding interest, ever. APRs range from 10% to 30%, depending on credit profiles.

Customizable Terms: Consumers can choose repayment periods between 3 and 48 months, providing flexibility to match their financial needs.

This model has powered Affirm’s growth, supporting:

17.3 million transactions as of late 2020.

$10.7 billion in Gross Merchandise Volume (GMV) facilitated through its platform.

Virtual Card

Not every retailer integrates Affirm directly, but the virtual card bridges this gap. Consumers can generate temporary cards through the Affirm app or website, enabling BNPL functionality at any retailer—online or offline.

Split Pay

Split Pay breaks smaller purchases (under $250) into four interest-free installments, making it ideal for high-frequency, low-ticket categories like groceries and apparel.

Affirm App and Marketplace

The Affirm app acts as a hub for payment management and merchant discovery.

32% of transactions in 2020 occurred via the app or marketplace.

Features like tailored financing offers and seamless repayment tools drive engagement, with over 4.8 million downloads to date.

High-Yield Savings Account

Affirm’s foray into consumer banking offers a 1% Annual Percentage Yield (APY) savings account with no fees or minimum deposits. This initiative complements its financing tools, building trust and promoting financial inclusivity.

Empowering Merchants

Affirm isn’t just a tool for consumers—it’s a strategic partner for merchants. Its suite of products helps businesses increase conversion rates, drive higher order values, and build customer loyalty.

Customizable Financing Options

Merchants can tailor financing offers, including 0% APR plans or interest-bearing loans. This flexibility lets businesses cater to diverse customer needs while boosting sales. Affirm’s merchants report:

92% higher average order values compared to traditional checkout.

20% increases in purchase approval rates.

Merchant Dashboard: Insights and Optimization

Affirm’s Merchant Dashboard provides real-time analytics, offering insights into metrics like:

Conversion rates.

Repeat purchase rates.

Customer segmentation and spending behavior.

These tools help merchants fine-tune their marketing strategies and maximize ROI.

Fraud Prevention and Support

Affirm’s fraud detection capabilities safeguard merchants, intercepting fraudulent activity before it impacts operations. Its Client Success Team works closely with businesses to interpret data and optimize performance.

Affirm’s product ecosystem doesn’t merely process payments—it builds trust on both ends of the transaction. Consumers get financial tools designed for clarity and ease, while merchants gain a partner that drives growth through innovation and insights.

As Affirm continues to refine its offerings and expand its reach, it cements its role as an indispensable component of the modern commerce stack—positioned not just to participate in the BNPL boom, but to lead it.

Business Model

Affirm operates as a dual-sided marketplace, seamlessly connecting consumers seeking transparent, flexible financing with merchants aiming to drive higher sales and loyalty. At its core, Affirm’s business model balances the needs of both sides, underpinned by innovative revenue strategies, advanced risk management, and scalable operations.

Here’s a closer look at how Affirm’s machine runs—and why it works.

Revenue Streams: Diversified and Strategic

1. Merchant Fees: The Engine of Growth

Merchants partner with Affirm to offer flexible payment options at checkout. In return, Affirm charges a percentage of the transaction value—typically between 3-8%, depending on the partnership.

Why Merchants Pay: Affirm helps solve key e-commerce pain points:

Higher conversion rates by making purchases more affordable.

Up to 92% higher average order values (AOV).

Reduced cart abandonment and increased repeat purchases.

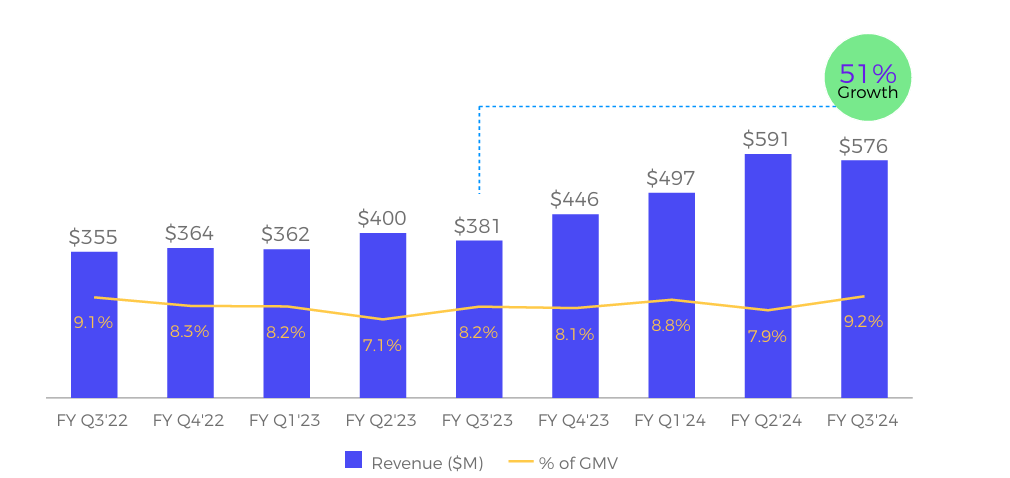

Impact: In FY2020, 64% of Affirm’s total loans originated from repeat customers, showcasing its ability to create long-term value for merchants.

2. Consumer Interest Income: Transparency at a Price

Affirm generates revenue from interest-bearing loans with APRs ranging from 10-30%. Unlike traditional credit cards, Affirm’s loans feature simple interest with no hidden fees or compounding.

Significance: In FY2020, 43% of Affirm’s revenue came from interest income, highlighting its role as a critical revenue driver.

This dual revenue model—combining merchant fees and consumer interest—creates a balanced, diversified income stream.

Cost Structure: Managing Risk and Scaling Effectively

Affirm’s operational costs are laser-focused on enabling its services while managing risk and maintaining scalability.

1. Funding the Loans

Affirm underwrites its loans through a mix of debt facilities and securitizations, raising over $1.6 billion to date. Access to low-cost capital allows Affirm to offer competitive terms to consumers while protecting margins.

2. Credit Risk Management

Affirm uses machine learning models to evaluate creditworthiness in real-time, minimizing defaults while approving loans efficiently.

Its net charge-off rates remain within industry standards, reflecting disciplined risk management.

3. Investment in Technology

Affirm’s tech stack enables seamless integrations with merchants while delivering a frictionless user experience for consumers. This investment fuels both scalability and innovation.

The Affirm Flywheel

Affirm’s business thrives on a virtuous cycle of network effects that amplify its value on both sides of the marketplace.

Consumer Side

As more merchants adopt Affirm, consumers encounter its financing options at more checkout points. Tools like the Affirm app and virtual card expand access, driving repeat usage and engagement.

Merchant Side

As consumer adoption grows, merchants see increased conversions and larger transaction volumes, incentivizing further partnerships. Affirm’s merchant dashboard offers insights into customer behavior, improving marketing efficiency and ROI.

This interplay between consumer and merchant incentives creates a powerful growth loop, allowing Affirm to scale rapidly.

Scalability

Affirm’s asset-light model facilitates growth while managing risk effectively.

1. Loan Funding Strategy

Affirm originates loans but sells 70-80% of them to institutional investors, transferring most of the credit risk off its balance sheet. This strategy frees up capital for further expansion.

2. Operating Leverage

Investments in technology and analytics create significant operating leverage. As transaction volumes grow, costs per transaction decrease, driving margin expansion over time.

Affirm’s Business at a Glance

Metric | Value (FY2020) |

|---|---|

Revenue | $509.5M, up 93% YoY |

Merchant Fees | ~57% of total revenue |

Consumer Interest Income | ~43% of total revenue |

GMV | $10.7B, up from $2.6B in FY2019 |

Repeat Loans | 64% of total loans |

Loan Sell-Through Rate | 70-80% |

Merchant Value Proposition

Merchants are at the heart of Affirm’s revenue model, drawn by its ability to:

Increase Conversions: 20% higher approval rates compared to traditional financing.

Boost AOV: Up to 92% higher with Affirm-enabled transactions.

Provide Insights: Real-time analytics to optimize CAC and marketing strategies.

Reduce Risk: Affirm absorbs default risk, ensuring merchants are paid in full.

Consumer Value Proposition

For consumers, Affirm offers a compelling alternative to traditional credit:

Transparent terms with no hidden fees or penalties.

Flexible repayment plans ranging from 3 to 48 months.

Accessibility for users with less-than-perfect credit, making financial inclusion a reality.

These features resonate particularly with younger demographics, with Millennials and Gen Z comprising the majority of Affirm’s user base.

Affirm: The Bridge Between Consumers and Merchants

At its core, Affirm isn’t just a payments company—it’s a trust engine for the modern financial ecosystem. By aligning consumer needs with merchant goals, Affirm has built a dual-sided marketplace that is indispensable in today’s commerce landscape.

The combination of transparency, scalability, and data-driven decision-making positions Affirm not just as a leader in BNPL but as a critical player in shaping the future of financial transactions.

Management Team:

Affirm’s leadership team is a blend of industry veterans with deep expertise in fintech, technology, and strategy. Their combined efforts ensure Affirm’s position as a leader in the Buy Now, Pay Later (BNPL) space.

Max Levchin – Founder, Chairman, and CEO

A co-founder of PayPal, Max Levchin is a fintech pioneer known for his innovative approach to financial systems. At Affirm, he focuses on building trust and transparency in consumer finance. Under his leadership, Affirm has formed major partnerships and scaled its Gross Merchandise Value (GMV) to $10.7 billion in FY2020, while successfully navigating its IPO.

Michael Linford – Chief Financial Officer (CFO)

Michael Linford brings extensive experience in financial strategy and scaling businesses, previously serving as CFO at HP Enterprise Software. At Affirm, he oversees financial planning and investor relations, playing a key role in the company’s IPO. His guidance helped Affirm achieve FY2020 revenue of $509.5 million.

Libor Michalek – President of Technology

With a background as a former Google and YouTube executive, Libor Michalek specializes in scalable systems and machine learning. At Affirm, he leads engineering and product development, spearheading innovations in underwriting models and fraud detection that ensure the platform’s reliability and security.

Investors and Ownership

Affirm's Investment Rounds

Seed Round (2012):

Affirm raised $3.5 million from Founders Fund, Khosla Ventures, and its founder Max Levchin. The funds were used to establish the company and develop its core BNPL product.Series A (2014):

Affirm secured $45 million in a Series A round led by Khosla Ventures, with participation from Lightspeed Venture Partners and Nyca Partners. This funding was allocated toward expanding its merchant partnerships and scaling product offerings. The company’s valuation at this stage was estimated at $200 million.Series B (2015):

In May 2015, Affirm raised a substantial $275 million, led by Spark Capital, with contributions from Andreessen Horowitz, Founders Fund, and Lightspeed Venture Partners. This round positioned the company with an estimated valuation of $800 million as it focused on onboarding more merchants and increasing transaction volumes.Series C (2017):

Affirm raised $100 million in its Series C round, led by Founders Fund and GIC, marking a pivotal milestone as the company reached a valuation of $1.75 billion, achieving unicorn status. The funding was allocated to enhancing Affirm’s underwriting technology and expanding into verticals like travel and fitness.Series D (2019):

Affirm raised $300 million in its Series D round led by Thrive Capital, with GIC, Lightspeed Venture Partners, and Fidelity Investments also participating. This brought the company’s valuation to $2.9 billion. The funds supported product diversification, including the launch of a high-yield savings account.Series E (2020):

The Series E round in September 2020 raised $500 million, led by GIC and Durable Capital Partners. Other participants included Baillie Gifford, Founders Fund, and Wellington Management. The round valued Affirm at $3.9 billion and facilitated its integration with Shopify, expanding its reach significantly in the e-commerce space

Debt Financing

In addition to equity funding, Affirm secured substantial debt to support its loan portfolio:

2018: $300 million from institutional lenders.

2020: $400 million through securitized loans, ensuring its ability to scale consumer lending operations.

IPO (2021)

Affirm went public on the Nasdaq in January 2021, raising $1.2 billion at an IPO valuation of $11.9 billion. Shares were priced at $49, and prominent investors such as Founders Fund, Lightspeed Venture Partners, and GIC retained significant stakes. The IPO marked Affirm’s maturity as a leader in the BNPL market.

Total Capital Raised (Pre-IPO):

Affirm raised over $1.6 billion in equity financing and $700 million in debt financing, which provided the foundation for its rapid growth and operational scaling.

Competition

Affirm operates in a competitive BNPL market against giants like Klarna, Afterpay, and PayPal. Klarna, with operations in over 17 countries and $53 billion GMV in 2020, leads in Europe through its expansive merchant network, including H&M and ASOS. Afterpay, popular among Millennials and Gen Z, focuses on fashion and beauty retail, processing $15.4 billion GMV in FY2020. Meanwhile, PayPal leverages its 426 million users and merchant relationships to scale its "Pay in 4" BNPL solution, integrating it seamlessly into its $310 billion quarterly payment volume in 2020.

Affirm distinguishes itself with transparency, no hidden fees, and strong partnerships with brands like Peloton, Shopify, and Expedia. Its access to Shopify’s $175 billion annual GMV network and proprietary machine learning models for credit risk assessment bolster its competitive edge. Focused on North America and high-ticket purchases in fitness, travel, and home improvement, Affirm thrives in a BNPL market set to grow from $120 billion in 2020 to $3.2 trillion by 2030. By prioritizing trust and innovation, Affirm solidifies its position as a leader in the industry.

Financials

Affirm's journey as a public company from 2021 to 2024 has been defined by rapid revenue growth, expanding partnerships, and aggressive investments in scaling its platform. While the company has yet to achieve profitability, its ability to generate significant Gross Merchandise Volume (GMV) and maintain strong liquidity underscores its potential to lead the Buy Now, Pay Later (BNPL) market.

2021: A Strong Debut

Affirm’s first year as a public entity showcased remarkable growth, driven by the rising adoption of BNPL services.

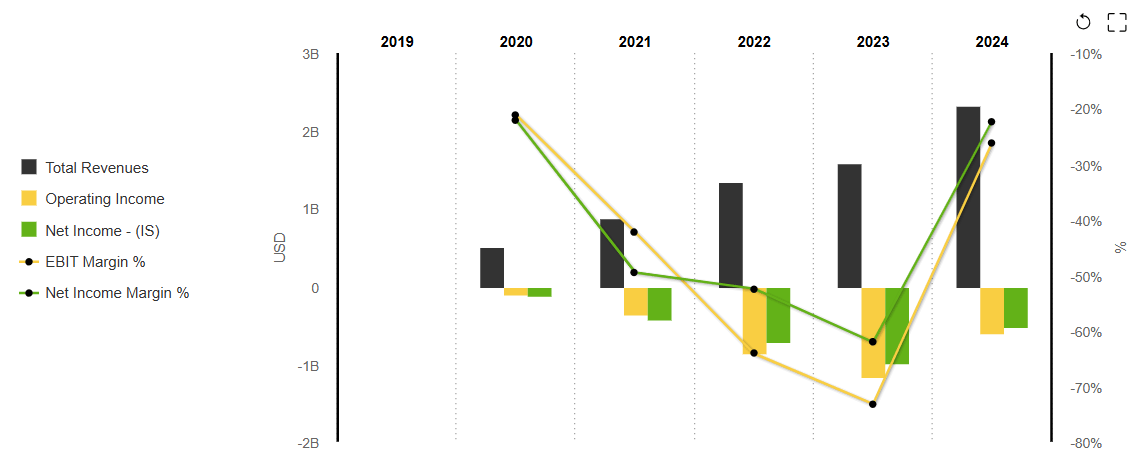

Revenue Growth: Affirm generated $870 million in revenue, marking a 70% year-over-year (YoY) increase.

GMV Expansion: Gross Merchandise Volume surged to $7.1 billion, an 80% YoY increase, reflecting strong consumer adoption.

Key Drivers: Partnerships with major players like Walmart and Shopify allowed Affirm to tap into broader consumer bases, bolstering its growth.

However, the company faced mounting challenges:

Net Losses: Affirm reported a net loss of $112.7 million, reflecting high marketing and operational costs.

Operating Expenses: Marketing and sales expenses more than doubled to $342 million, underscoring the aggressive push for customer acquisition.

Liquidity: Despite these losses, Affirm maintained a strong liquidity position with $1.1 billion in cash and equivalents, ensuring its capacity for future growth.

2022: Growth Continues, But Losses Deepen

Affirm built on its momentum in 2022, achieving significant revenue growth while grappling with higher operating costs.

Revenue Growth: Revenue increased to $1.2 billion, a 38% YoY rise.

GMV: Gross Merchandise Volume reached $10 billion, a 40% YoY increase, signaling robust demand for BNPL services.

Partnerships: Affirm continued to expand its merchant network, leveraging relationships with major retailers to drive adoption.

Despite these gains, the financial picture darkened:

Net Losses: Losses widened to $387.5 million, as Affirm invested heavily in customer acquisition and technology infrastructure.

Marketing Spend: Marketing expenses surged to $425 million, reflecting Affirm’s efforts to maintain its growth trajectory.

Assets and Liabilities: Total assets grew to $5.7 billion, while liabilities increased to $3.1 billion, primarily due to funding loan growth.

2023: Revenue Soars, but Losses Peak

2023 was marked by Affirm’s continued revenue growth but also its most significant annual loss.

Revenue Growth: Affirm’s revenue rose to $1.8 billion, a 50% YoY increase.

GMV: Gross Merchandise Volume climbed to $14.2 billion, continuing its upward trend.

Strategic Growth: Partnerships with e-commerce platforms and the expansion of its merchant portfolio drove increased consumer engagement.

However, profitability remained elusive:

Net Losses: Losses widened to $900 million, reflecting the high costs of scaling operations, marketing, and infrastructure.

Operating Expenses: Marketing and R&D investments remained elevated, straining margins.

Liquidity: Operating cash flow reached $500 million, ensuring Affirm’s ability to fund ongoing growth.

2024: Optimized Operations and Improved Losses

In 2024, Affirm demonstrated signs of operational improvement, balancing growth with more disciplined cost management.

Revenue Growth: Revenue reached $2.3 billion, a 28% YoY increase, fueled by expanded consumer and merchant partnerships.

GMV: Gross Merchandise Volume grew to $17.5 billion, a 20% YoY increase.

Net Loss Improvement: Losses decreased to $450 million, reflecting better efficiency in customer acquisition and marketing spend.

Liquidity: Operating cash flow grew to $550 million, bolstering Affirm’s financial stability.

Assets and Liabilities: Total assets increased to $7.5 billion, while liabilities rose to $4 billion, tied to the continued expansion of its loan portfolio.

Key Metrics (2021–2024)

Metric | 2021 | 2022 | 2023 | 2024 |

|---|---|---|---|---|

Revenue | $870M | $1.2B | $1.8B | $2.3B |

Net Loss | $112.7M | $387.5M | $900M | $450M |

GMV | $7.1B | $10.0B | $14.2B | $17.5B |

Cash Flow (Op.) | $1.1B | $400M | $500M | $550M |

Assets | $4.5B | $5.7B | $6.4B | $7.5B |

Liabilities | $2.2B | $3.1B | $3.8B | $4.0B |

Affirm’s growth trajectory underscores its ability to capitalize on the expanding BNPL market, with revenue and GMV increasing year-over-year. However, profitability remains a challenge, driven by high operating costs and aggressive investments in marketing and technology.

The company’s improved cost management in 2024 and strong liquidity position offer optimism for a more sustainable financial future. As Affirm refines its operational model and expands its reach, it remains a critical player in reshaping consumer finance and the e-commerce landscape.

Closing thoughts

Affirm’s journey from 2021 to 2024 showcases a company navigating the rapid growth of the Buy Now, Pay Later (BNPL) market while grappling with the challenges of achieving profitability. Over these four years, Affirm has successfully expanded its revenue base and merchant network, solidifying its position as a leader in the financial technology space. The company’s Gross Merchandise Volume (GMV) has consistently risen, reflecting growing consumer and merchant adoption of its transparent, flexible financing solutions.

Despite these successes, Affirm’s financial story is one of trade-offs. The company’s aggressive growth strategy, marked by substantial investments in marketing, technology, and customer acquisition, has come at the cost of mounting net losses. However, 2024 signaled a turning point, with Affirm demonstrating improved cost management and a significant reduction in losses. This progress, coupled with strong liquidity and operating cash flow, positions the company to better balance growth with financial sustainability.

Looking ahead, Affirm’s ability to maintain its competitive edge will depend on its execution in key areas. Continued innovation in product offerings, such as expanding into everyday spending categories and new verticals like healthcare and education, presents significant opportunities. Additionally, international expansion could unlock new markets and drive further growth. However, the path to sustained profitability will require Affirm to optimize its operating model while addressing rising competition and economic headwinds.

In a market undergoing a generational shift in consumer credit, Affirm is not just keeping pace—it’s helping to define the landscape. By prioritizing transparency and trust, Affirm has positioned itself as more than a financial services provider; it’s a partner for consumers and merchants navigating the future of commerce. With strong fundamentals and a clear vision, Affirm’s long-term potential remains promising, even as it works toward financial equilibrium.

Here is my interview with Anand Chandra, the founder of Arya.ag, India’s largest grain commerce platform which bridges the gap between sellers and buyers of agriproducts, providing complete assurance on quantity, quality, and payments.

If you enjoyed our analysis, we’d very much appreciate you sharing with a friend.

Tweets of the week

Here are the options I have for us to work together. If any of them are interesting to you - hit me up!

Amplify Labs: We help you grow your audience on LinkedIn, X (formerly Twitter), and newsletters.

Subscribe to my YouTube channel: Your Learning Playground with over 350+ podcasts. Previous guests include Guy Kawasaki, Brad Feld, James Clear, and Shu Nyatta.

Sponsor this newsletter: Reach thousands of tech leaders

And that’s it from me. See you next week.